Introduction

MiFID II transaction reporting, governed under MiFIR, has been in place for several years.

Most firms now operate established processes aligned with MiFID II requirements, with systems that consistently submit reports on time.

However, regulatory focus has shifted beyond submission.

Supervisors now expect firms to demonstrate the accuracy of every reported field and clearly explain how each data point was sourced, calculated, validated, and mapped from underlying systems.

This shift is evident in FCA supervisory expectations and ESMA MiFIR data quality guidance. Firms must now prove not only that reports were submitted, but that the data within them is correct.

The challenge is no longer operational. It is evidential.

Reports may be submitted and accepted by ARMs yet still contain errors. These issues often surface only when firms are required to justify specific fields, logic, or mappings. In many cases, this demands investigation across multiple systems, teams, and data sources.

The real issue is not the ability to report, but the ability to explain and defend what has been reported field by field under regulatory scrutiny.

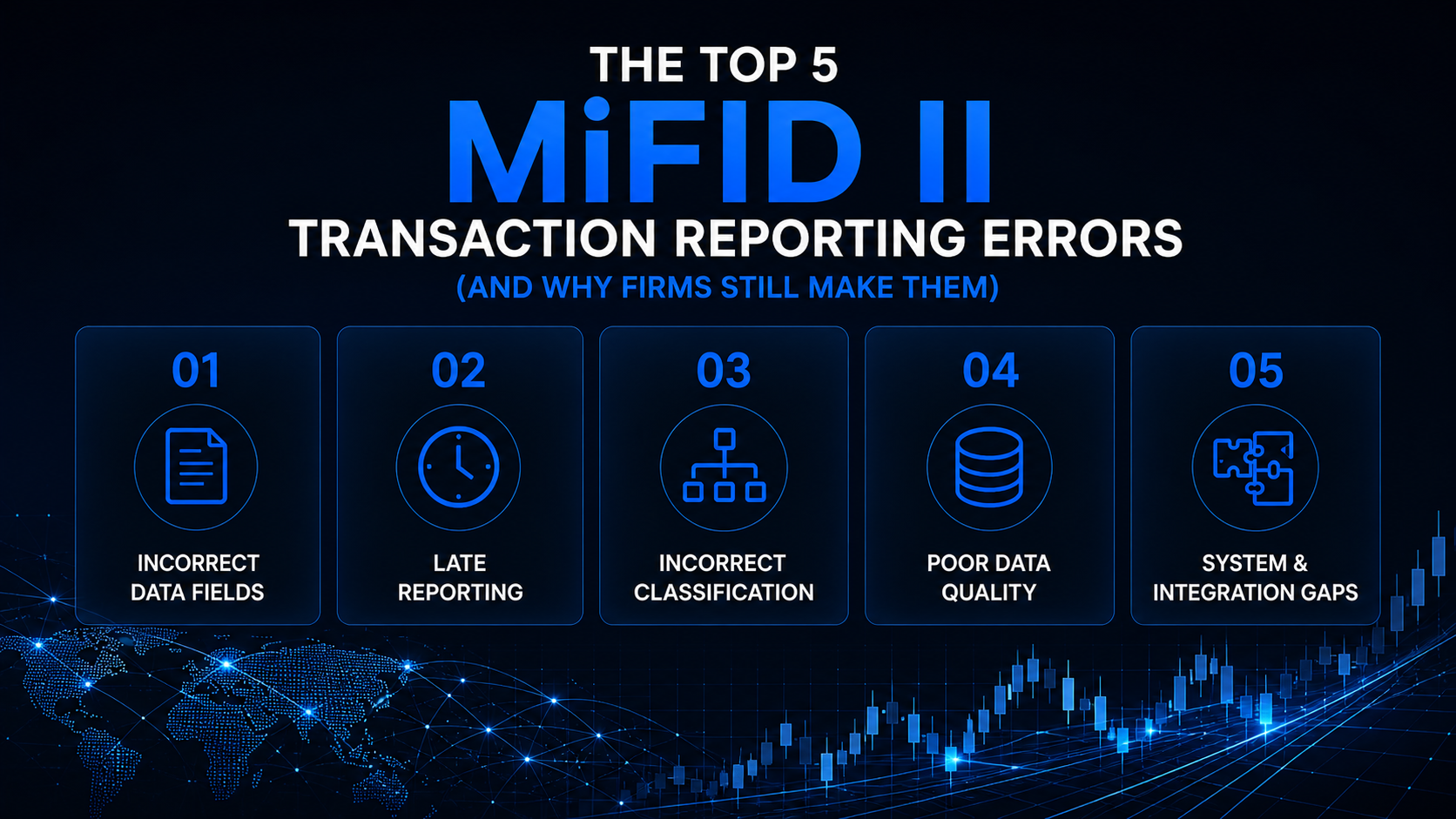

Where MiFID II Reporting Controls Break Down

1. Assuming Accepted Reports are Correct

Why this happens:

Firms often treat ARM acceptance as validation. Once a report passes schema and format checks, it is considered complete. Over time, acceptance becomes a proxy for correctness.

What it reveals:

Validation rules confirm structure, not accuracy.

A report can be accepted while still containing incorrect field-level data. This becomes apparent when firms are asked to explain specific fields but cannot clearly demonstrate how values were sourced, calculated, or mapped.

This is where process-level controls fail to deliver regulator-grade assurance.

2. Relying on Sampling Instead of Full Population Testing

Why this happens

Given the volume of reporting, firms often rely on sampling to assess data quality.

What it reveals:

Sampling provides partial assurance, not complete coverage.

Errors outside the sample remain undetected, even when they affect large portions of the reporting population.

Regulators expect firms to stand behind every reported transaction, not just a subset. Sampling may create confidence, but it does not provide defensibility.

3. Weak Reconciliation Between Front Office and Reported Transactions

Why this happens

Reconciliation processes are often periodic, limited in scope, or focused on high-level comparisons rather than full transaction-level alignment.

What it reveals:

Gaps between front office records and reported transactions can result in missing trades, duplicate submissions, or inconsistent data.

These issues are not always visible through standard controls and are increasingly identified during regulatory reviews.

The real challenge is not detecting that something is wrong. It is proving that everything is correct.

4. Inconsistent Reporting Logic Across Systems

Why this happens:

Reporting logic is distributed across systems, jurisdictions, and teams. Over time, inconsistencies in interpretation and implementation emerge.

What it reveals:

Inconsistent logic produces outputs that cannot be explained uniformly.

When firms are asked how a field was derived, responses vary depending on the system or data source. This signals a breakdown in control over reporting logic, not just data quality

5. Lack of Field-Level Transparency

Why this happens:

Most reporting systems are designed to generate outputs, not provide traceability.

What it reveals:

When issues arise, firms rely on manual investigations to trace data lineage across systems. This delays resolution and weakens their ability to demonstrate control.

The challenge is not correcting errors. It is evidencing how those errors were identified and why they occurred.

What These Errors Have in Common

Each of these issues reflects the same underlying gap.

Firms rely on processes that confirm reports were submitted but cannot independently demonstrate that the data within those reports is correct.

Regulators are increasingly focused on this distinction. Acceptance and validation are no longer sufficient. Firms must demonstrate how data is sourced, transformed, and validated across the entire reporting population.

This leads to a critical question:

If your firm were asked today to evidence the accuracy of a specific field across all reported transactions, could that evidence be produced immediately or would it require investigation?

If it requires investigation, the control has already failed.

This is not theoretical. It reflects how control frameworks are currently being tested in supervisory reviews.

How Reg-X Helps Address These Control Gaps

Reg-X strengthens MiFID II reporting controls by introducing an independent layer that validates data accuracy at the field level. It operates alongside existing systems and integrates with current reporting and reconciliation infrastructure without requiring replacement.

What Reg-X Is Not

Reg-X is not a reporting system, reconciliation tool, or validation engine.

These components already exist and support reporting workflows. However, they are not designed to independently prove whether each reported field is correct across the full transaction population, especially under regulatory scrutiny.

This explains why firms can have multiple control layers in place yet still struggle to explain how specific data points were derived, validated, and reported.

Why Existing Solutions Are Not Enough

Most firms already maintain validation, reconciliation, and reporting controls:

Validation confirms format .

Reconciliation compares datasets.

Reporting systems handle submission.

None of these prove that reported data is correct at a field level across all transactions.

As a result, issues often surface only when firms are asked to explain specific data points, not at the point of submission.

The limitation is structural. These controls were not designed to provide regulator-grade evidence of accuracy.

Where Reg-X Sits

Reg-X sits above existing control layers, testing the outputs they produce.

It provides an independent view of whether reported data is accurate, complete, and explainable across the full reporting population. It also enhances visibility into reconciliation outcomes, enabling firms to identify root causes rather than simply detect discrepancies.

Most firms already have multiple control layers. What they typically lack is one that validates accuracy at this level of detail.

RegAssure Accuracy

RegAssure Accuracy tests data across the full reporting population:

- Covers 100% of transactions and fields

- Eliminates reliance on sampling

- Identifies errors that pass validation

- Provides field-level diagnostics and traceability

This enables firms to move from assumed accuracy to evidenced accuracy.

RegAssure Completeness

RegAssure Completeness ensures reporting completeness:

- Compares front office records with reported transactions

- Identifies missing and duplicate trades

- Ensures full coverage of in-scope reporting obligations

What This Changes

This shifts control frameworks from process validation to data validation.

Instead of relying on submission, reconciliation, or sampling, firms gain full-population visibility into whether their data is truly correct.

Without this layer, firms depend on controls that appear robust but fail under detailed regulatory testing.

It also enables firms to identify and remediate historical reporting issues before they are exposed externally.

As expectations evolve, this level of validation is becoming essential for a defensible MiFID II reporting framework.

Why This Matters Now

Regulatory expectations have evolved.

The focus is no longer on whether reports were submitted. It is on whether firms can prove the data is correct.

This is already being tested in supervisory reviews. Firms that cannot clearly evidence their data are exposed under scrutiny.

The risk is not just that errors exist. It is that they are identified externally before they are understood internally.

MiFID II compliance is now defined by the ability to demonstrate data accuracy, not just reporting completeness.

Final Thought

Most firms have built robust reporting processes. The more pressing question is whether those processes are supported by equally robust control frameworks.

Can your firm evidence that every reported field is correct?

Can you demonstrate that all transactions have been accurately reported?

Can you clearly explain how your data is sourced, mapped, and validated?

These are the questions regulators are already asking and increasingly expect to be answered immediately.

Most firms have multiple control layers, but these were not designed to provide independent evidence of accuracy across the full reporting population.

Firms that are ahead are already testing their frameworks at this level. Others rely on investigation when questions arise.

If your framework falls into the latter category, it is unlikely to withstand detailed regulatory scrutiny today.

If evidence cannot be produced without investigation, the gap already exists. It simply has not yet been exposed.

At that point, the question is no longer whether a gap exists, but when it will be identified.

Speak with the Reg-X team to assess how your MiFID II reporting controls would stand up under regulatory scrutiny.